Overview

Risk management is how you control what you lose when a trade goes wrong; position sizing is how much you put on each trade. Together they are the most important skill in trading — more decisive to your results than any entry signal.

The logic is simple and unforgiving: you can't control whether a trade wins, but you can completely control how much it costs you when it loses. Everything else is secondary to staying in the game.

Origins & history

- 1956John L. Kelly, a scientist at AT&T Bell Labs, derived the Kelly criterion — the bet size that maximizes long-run growth given an edge. It crossed from information theory into gambling and then trading.1

- RootsThe deeper idea — risk of ruin — comes from centuries of gambling mathematics: bet too big relative to your edge and eventual bankruptcy becomes a near-certainty.2

- ModernVan Tharp popularized the term “position sizing” and argued, with simulations, that it — not entries — is the dominant driver of trading performance.3

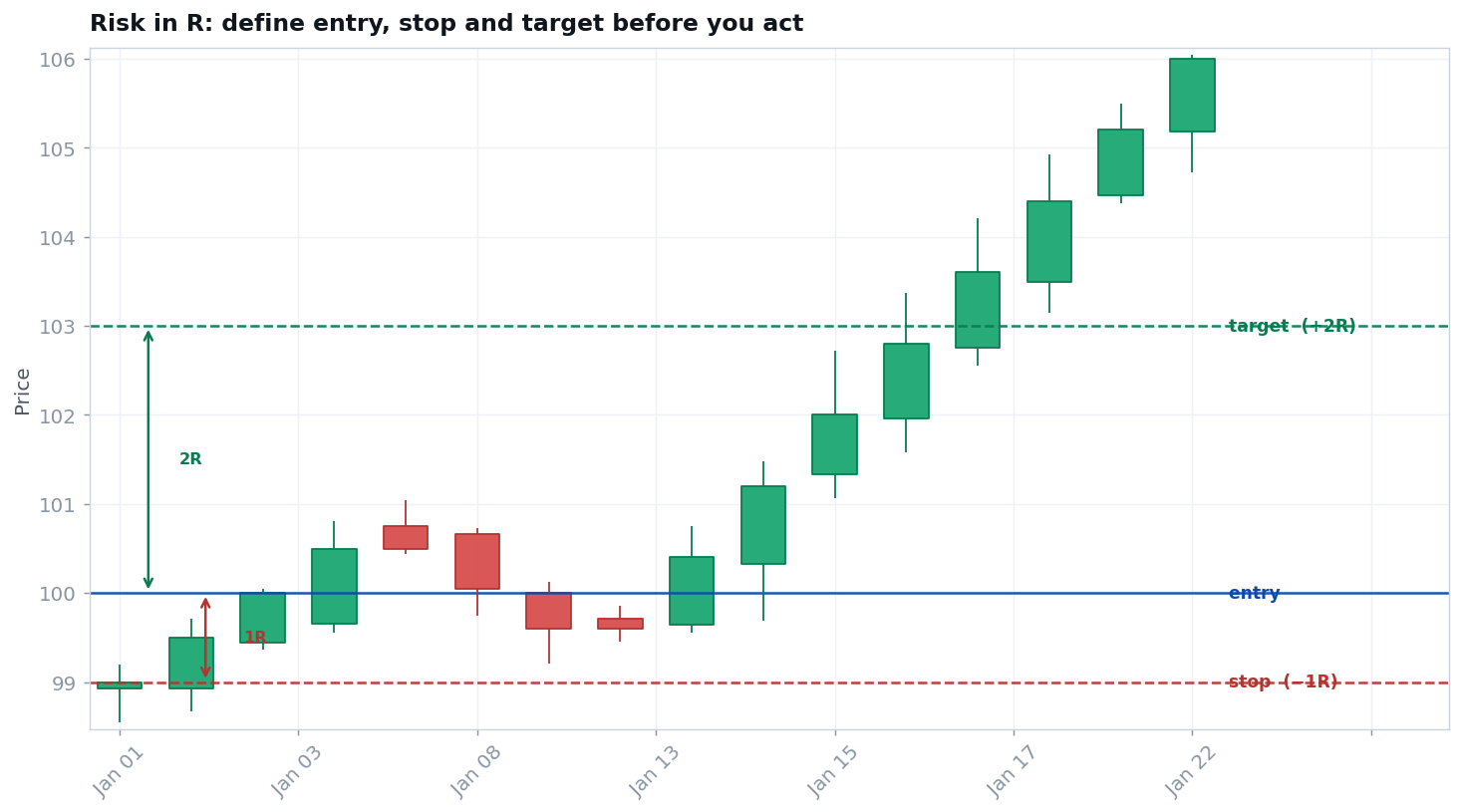

How it works

The professional sequence is always the same — decide the loss first:

This fixed-fractional approach means a tighter stop allows more shares and a wider stop fewer — the dollar loss stays constant. Two more numbers govern the long run:

And the reason small losses matter so much is the asymmetry of recovery: a 50% loss requires a 100% gain just to break even, and a 90% loss requires 900%.

Market psychology & mechanics

Risk rules exist to remove emotion from the moment it does the most damage. By defining the stop and the size before entering, you convert a frightening live decision into a number you already accepted. Fixed-fractional sizing also de-risks automatically: as the account shrinks in a drawdown, the dollars risked shrink too, slowing the bleeding exactly when you're most fragile. The opposite — adding to losers, sizing up to “win it back” — is how accounts reach risk of ruin.

Honest assessment

Strengths

It is the one variable entirely within your control. A trader with only a mediocre edge but excellent risk control can survive and compound; a trader with a great edge and poor risk control eventually blows up. Survival is the prerequisite for everything else.

The evidence

The mathematics is not in dispute: the Kelly criterion provably maximizes long-run logarithmic growth for a known edge, and risk-of-ruin formulas show how oversizing guarantees eventual ruin. Van Tharp's position-sizing simulations demonstrate that sizing accounts for far more of the variation in results than the entry method does.1

Evidence rating: the strongest, most rigorously grounded area in all of trading — this is math, not opinion.

Weaknesses & failure modes

- FULL KELLYFull Kelly is too aggressive. It maximizes growth but produces brutal 50%+ drawdowns; almost everyone uses half-Kelly or less.1

- GARBAGE INYou must know your edge. Kelly and expectancy depend on accurate win-rate and payoff estimates; overestimate your edge and you over-bet.

- CORRELATIONCorrelation hides exposure. Five “1% risk” trades in correlated names can be one 5% bet in disguise.

- TAILStops can gap. A stop is not a guarantee — gaps and slippage can make a loss larger than planned, so size for the worst realistic day.

Professional uses vs. retail misuses

How professionals do it

- Decide the loss first, then size to it — fixed-fractional, small.

- Use fractional Kelly and account for correlation and tails.

- Layered limits — per trade, per day, per week (see the desk rules).

Common retail mistakes

- No stop, or sizing by gut rather than by risk.

- Averaging down / martingale — adding to losers.

- Risking far too much per trade, courting risk of ruin.

Going deeper

Methods: fixed-fractional vs. fixed-ratio sizing, the Kelly criterion and fractional Kelly, R-multiples and expectancy, risk of ruin, drawdown recovery math, and portfolio “heat” (total open risk across correlated positions). Multi-timeframe: the same 1% rule scales from a scalper's many small bets to a position trader's few large ones — the percentage stays constant, the trade frequency and stop distance change.

Practice

Quiz 1 — Why is position sizing often called more important than your entry?

Because it controls the magnitude of every outcome. A great entry method with oversized bets still leads to ruin in a normal losing streak; a modest edge with disciplined sizing survives and compounds. Sizing drives most of the variation in results.

Quiz 2 — You're down 50%. What gain do you need to break even?

100%. Recovery is asymmetric — the deeper the hole, the disproportionately larger the climb (a 90% loss needs a 900% gain). That's why keeping losses small is everything.

Quiz 3 — Why do most traders use a fraction of the Kelly bet?

Full Kelly maximizes growth but produces severe drawdowns and assumes you know your edge precisely. Because edge estimates are uncertain, half-Kelly (or less) is far safer for the same broad benefit.

This concept in the knowledge graph

Resources

- COURSEThe desk-rules system — layered loss limits in practice.

- GLOSSARYPosition sizing, stop-loss, expectancy, drawdown.